Probably Wrong

Stochastic Contamination: The Case Against Probabilistic AI in Financial Data Processing

Author: Lucy Cohen

Abstract

The deployment of large language models and probabilistic AI systems in financial services is accelerating. Regulators are responding with governance frameworks that address transparency, explainability, and bias. None of the frameworks currently in force, including the EU AI Act, the Financial Conduct Authority’s guidance on AI in financial services, the Financial Reporting Council’s audit standards, the IAASB’s International Standards on Auditing, PCAOB oversight requirements, HMRC’s Making Tax Digital framework, or Companies House filing standards, prohibits the use of probabilistic AI in financial data processing on architectural grounds. This paper argues that they should, and provides the theoretical and empirical basis for that prohibition.

This paper introduces the concept of Stochastic Contamination: the irreversible introduction of probabilistic uncertainty into a data system whose integrity depends on deterministic verifiability. Financial data is not information in the general sense - it constitutes a system of constrained truth claims governed simultaneously by mathematical conservation laws, legal obligations of accuracy, and audit verifiability requirements. This paper formalises these properties as the Financial Epistemic Integrity condition and demonstrates that it is incompatible, at the architectural level, with the output properties of any probabilistic generative system.

This paper states and proves the Stochastic Contamination Theorem: that any probabilistic AI system operating on financial data introduces uncertainty that is undetectable at the point of introduction, unverifiable without complete re-derivation from source data, and therefore irrecoverable within any audit or compliance framework that does not itself have access to those source data in their entirety. The paper further demonstrates that the properties of transformer-based large language models, including token-level stochastic sampling, attention-weighted context compression, and the absence of a traceable logical derivation chain between input and output, produce contamination that cannot be corrected by retrieval augmentation, fine-tuning on financial corpora, or constitutional constraint mechanisms. The disqualification is architectural, not operational.

The paper draws on empirical evidence from a live deployment of a deterministic financial processing system across UK micro-businesses, in which contamination-free processing produced a defect rate of zero against materiality thresholds, while probabilistic-adjacent human-assisted processing introduced errors at rates consistent with documented manual processing failure rates. The argument extends to the systemic implications: contaminated financial data propagating into statutory audit, published financial statements, tax submissions to HMRC and Companies House, stock market valuations, credit ratings, and macroeconomic accounting. The paper proposes a minimum property set, the Financial AI Fitness Standard, that any AI system must satisfy before operating on financial data, and identifies the specific amendments required across each regulatory framework to encode this standard into law.

The financial system depends on the integrity of the data that describes it. Probabilistic AI systems are incapable of preserving that integrity by design. The question is not whether this matters - because it does; it is whether regulators will act before the contamination becomes systemic.

Keywords: stochastic contamination, financial epistemic integrity, large language models, probabilistic AI, financial data integrity, audit, deterministic verification, AI governance, FCA, FRC, IAASB, PCAOB, HMRC, Companies House

1. Introduction

In 2024, Bloomberg reported that major financial institutions, including Morgan Stanley, JPMorgan, and Goldman Sachs were deploying large language model applications for client-facing analysis, document processing, and financial summarisation. In 2025, the Big Four accounting firms collectively committed billions of dollars to AI integration across audit, tax, and advisory functions. HMRC announced the progressive automation of compliance checking through AI-assisted data matching. The momentum is institutional, the investment is substantial, and the direction is clear: probabilistic AI is moving into financial data processing at scale.

The governance response has not kept pace. The EU AI Act classifies AI systems by risk domain and mandates transparency, explainability, and human oversight. The Financial Conduct Authority has published guidance requiring firms to ensure AI outputs are explainable and subject to appropriate controls. The Financial Reporting Council has acknowledged AI’s growing role in audit while reaffirming the primacy of auditor judgement. The IAASB and PCAOB are consulting on how existing audit standards apply to AI-assisted procedures. HMRC and Companies House accept digitally processed submissions without architectural requirements on the systems that produced them. Across every framework, the question being asked is how probabilistic AI should be governed in financial contexts. This paper argues that the question is wrong. The question that should be asked is whether probabilistic AI is architecturally capable of operating on financial data without corrupting it.

The answer this paper provides, formally and empirically, is that it is not.

The argument turns on a distinction that the governance literature has not yet made with sufficient precision: the distinction between information in the general sense and financial data as a special epistemic category. Information, in the general sense, tolerates approximation. A language model that produces a plausible summary of a news article, a persuasive draft of a contract, or a reasonable answer to a factual question may be useful even when it is imprecise, because the cost of imprecision is bounded and correctable. Financial data does not share this tolerance. A financial record is not a representation of approximate economic reality. It is a constrained truth claim that must simultaneously satisfy a mathematical conservation law, a legal obligation of accuracy enforceable by regulatory sanction, and an audit verifiability requirement that demands every figure be traceable to its source. Approximation in financial data is not imprecision. It is contamination.

This paper introduces the concept of Stochastic Contamination to name this phenomenon precisely. Stochastic Contamination occurs when a probabilistic generative system introduces uncertainty into a financial data system at a point where that uncertainty cannot subsequently be detected, isolated, or removed without complete re-derivation of the affected records from source data. The contamination is not merely a risk of error, but a structural property of the interaction between probabilistic output generation and the verifiability requirements that financial data must satisfy. It occurs whether or not the probabilistic system produces a correct output in any given instance, because the absence of a deterministic derivation chain means that correctness cannot be established without reference to information the system does not possess and cannot provide.

This paper puts forward several arguments:

Section 2 establishes the epistemic category of financial data formally, defining the Financial Epistemic Integrity condition and distinguishing financial data from other information types on mathematical, legal, and audit grounds.

Section 3 introduces the Stochastic Contamination framework, defining the concept precisely, establishing its conditions of occurrence, and demonstrating why contamination, once introduced, is irrecoverable within standard audit and compliance architectures.

Section 4 states and proves the Stochastic Contamination Theorem, which formalises the incompatibility between probabilistic AI output properties and the Financial Epistemic Integrity condition.

Section 5 applies the theorem specifically to large language models, examining why the architectural properties of transformer-based systems produce contamination that retrieval augmentation, domain fine-tuning, and constitutional constraint cannot resolve.

Section 6 surveys the regulatory landscape across the FRC, FCA, IAASB, PCAOB, HMRC, and Companies House, identifying precisely where each framework’s conceptual vocabulary is insufficient to detect or prohibit contamination and what amendment would close each gap.

Section 7 extends the argument to the systemic level, examining the propagation of contaminated financial data into statutory audit, published financial statements, capital market valuations, credit assessments, and macroeconomic accounting. Section 8 presents empirical evidence from a live deterministic financial processing deployment as proof of concept for the alternative architecture. Section 9 proposes the Financial AI Fitness Standard: a minimum property set, derived directly from the theorem, that any AI system must satisfy before operating on financial data.

The conclusion asks three things of the reader. First, to accept the Financial Epistemic Integrity condition as a real and consequential property of financial data that current governance frameworks have failed to formalise. Second, to accept the Stochastic Contamination Theorem as a mathematical fact about the interaction between probabilistic AI and that condition, subject to the proof offered in Section 4. Third, to accept that the Financial AI Fitness Standard proposed in Section 9 represents not an aspirational policy preference but the minimum requirement for AI governance in financial contexts to be something other than fiction.

The financial system is built on the assumption that the data describing it is trustworthy. Probabilistic AI systems cannot satisfy that assumption by design. Every day that assumption goes unexamined while probabilistic systems process financial data is a day in which the trustworthiness of that data erodes in ways that are, by the theorem proved in this paper, undetectable until after the damage is done.

2. Financial Data as a Special Epistemic Category

The governance literature on AI in financial services treats financial data as a high-stakes instance of data in general. The concern is that errors in financial data have large consequences, not that financial data has properties that make certain classes of error structurally different from errors in other domains. This conflation is the root of the regulatory gap identified in Section 1. Financial data is not high-stakes general information. It is a categorically distinct epistemic object, and the distinction has direct implications for what kinds of system may legitimately produce or process it.

This section establishes that distinction formally. We define three properties that together constitute the Financial Epistemic Integrity condition, demonstrate that each property is independently necessary for financial data to function as financial data, and show that the conjunction of all three creates a requirement for deterministic verifiability that no probabilistic generative system can satisfy.

2.1 The Mathematical Conservation Property

Financial data is governed by a conservation law with no analogue in general information systems. The fundamental accounting equation, expressed in its most general form as:

ΔAssets = ΔLiabilities + ΔEquity

is not a convention or a rule of practice. It is a mathematical identity that must hold across every state of a financial system at every point in time. Every financial record, every transaction, every reported balance is a claim about the state of a system subject to this constraint. A financial record that violates the conservation law is not an inaccurate record; actually, it is not a financial record at all. It has failed the minimum condition for membership in the class of objects to which financial data belongs.

This conservation property has a deeper formal structure than the surface equation suggests. Each transaction admitted into a financial system must preserve the conservation constraint across the entire state of that system, not merely within the account or ledger directly affected. A transaction that produces a locally correct entry while creating a global imbalance has not produced a financial record. It has produced a defect. The implication is that financial data processing is not a collection of independent record-keeping acts. It is a state-preserving operation across a constrained system, and the constraint must hold continuously, not merely at the point of reporting. In short, financial systems must balance at all times – and that is the condition on which the entire global financial ecosystem is built.

The conservation property has a further implication that is directly relevant to the contamination argument. Because the constraint must hold globally, a local error, one that affects a single transaction or a single account balance, propagates through the system until it is detected and corrected. A misclassified transaction does not remain locally contained. It produces an incorrect account balance, which produces an incorrect trial balance, which produces incorrect financial statements, which produces incorrect tax submissions, which produces incorrect regulatory filings. The propagation is total. This property, which we term conservation propagation, means that the cost of a financial data error is not bounded by the magnitude of the error at its point of introduction. It is bounded only by the reach of the financial system into which it propagates.

2.2 The Legal Obligation Property

Financial data carries a legal obligation of accuracy that distinguishes it categorically from most other information types. In the United Kingdom, the Companies Act 2006 requires that financial statements give a true and fair view of the company’s financial position and performance. HMRC requires that tax returns accurately reflect the underlying financial records. Companies House requires that filed accounts represent the company’s actual financial state. These are legally enforceable obligations backed by criminal sanctions for deliberate falsification and civil penalties for negligent inaccuracy.

The legal obligation property creates an epistemic requirement that goes beyond accuracy in the ordinary sense. A financial record must be demonstrably correct, in the sense that its correctness can be established through reference to verifiable source evidence if challenged by a regulator, an auditor, or a court. A financial record whose correctness cannot be demonstrated is a legally deficient record, regardless of whether it happens to be numerically accurate.

This demonstrability requirement has a structural form that the conservation property alone does not capture. A financial record must be derivable from accessible source evidence through a process that can be re-run, inspected, and confirmed by a third party operating independently of the system that produced it. A record whose numerical content is correct but whose derivation from source cannot be demonstrated fails this requirement as completely as a record that is numerically wrong. The correctness of the number is not the point. The verifiability of its derivation is.

2.3 The Audit Verifiability Property

The third property of financial data follows from and extends the first two. Every figure in a financial system must be traceable, through an unbroken chain of derivation, to primary source evidence: bank statements, invoices, contracts, payroll records, asset valuations, and similar documents that exist independently of the financial data system itself. This traceability requirement, which we term the audit trail condition, is the operational expression of the legal obligation property and the enforcement mechanism of the conservation property.

The audit trail condition has both a backward-looking and a forward-looking dimension. Backward-looking traceability means that any figure in a financial statement can be decomposed into the transactions that produced it, and each transaction can be traced to the source document that evidenced it. Forward-looking traceability means that any source document can be followed through the processing chain to identify every financial record it affected and every balance it contributed to. Together, these two dimensions create what the International Standards on Auditing describe as a complete and auditable record, a data system in which every number has a provenance and every provenance is accessible (IAASB, 2023).

The audit verifiability property creates a structural requirement for financial data processing that is distinct from the conservation and legal obligation properties, though related to both. A financial data processing system must not merely produce outputs that satisfy the conservation law and comply with legal accuracy obligations. It must produce outputs whose derivation is transparent, step-by-step, and traceable to source. The derivation chain is part of the financial record itself, without which the record fails the audit verifiability property and cannot be admitted into the verified financial state.

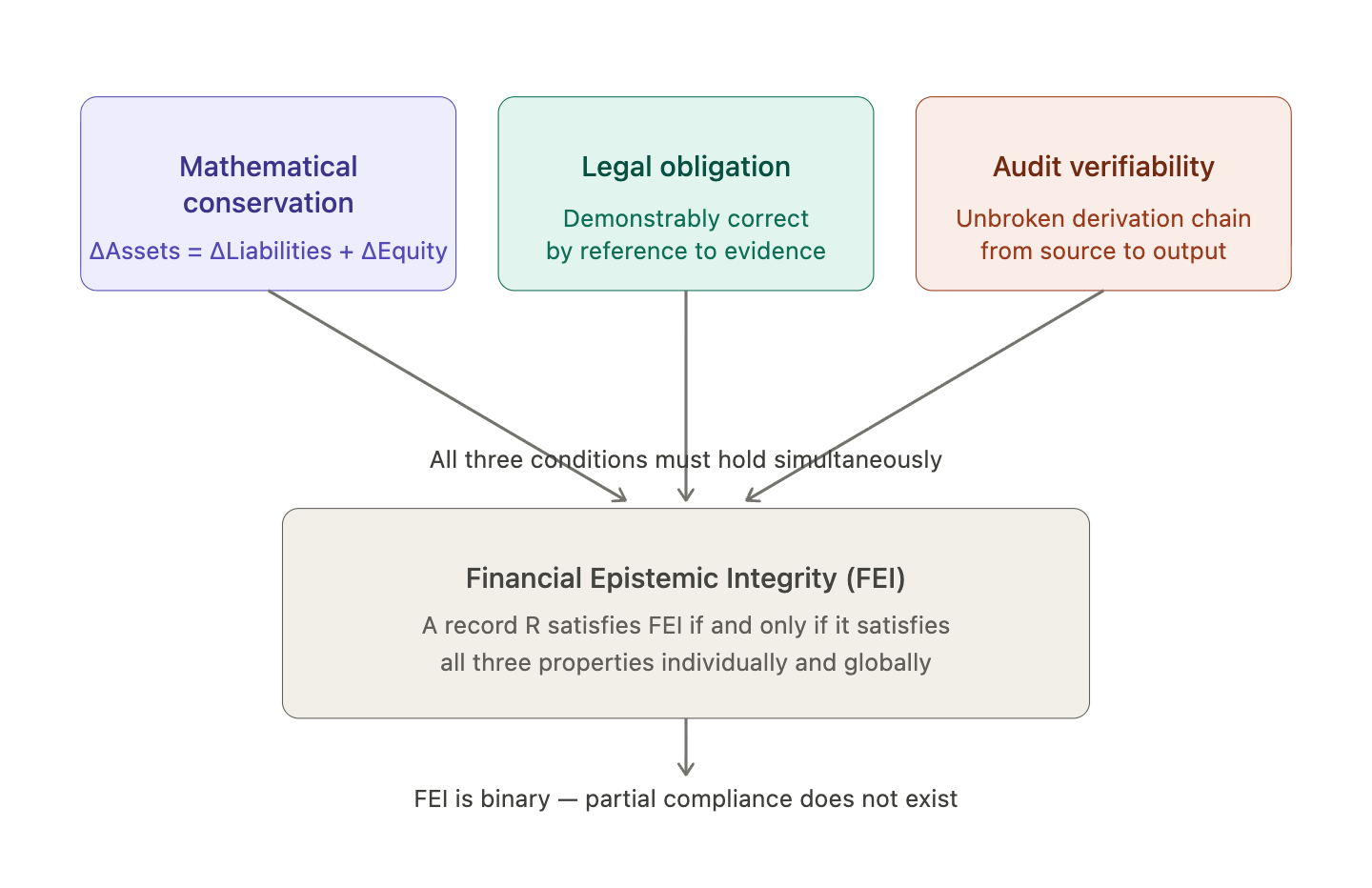

2.4 The Financial Epistemic Integrity Condition

The three properties established in Sections 2.1 through 2.3 jointly define what we term the Financial Epistemic Integrity condition. Formally:

A financial data record R satisfies Financial Epistemic Integrity (FEI) if and only if:

(i) R is consistent with the conservation constraint across the financial state system of which it forms part;

(ii) There exists a set of accessible and auditable source evidence E such that the correctness of R can be established by reference to E; and

(iii) The derivation of R from E is traceable through an unbroken, step-by-step chain that is itself auditable.

A financial data system satisfies FEI if, and only if, every record within it satisfies FEI individually, and the conservation constraint holds globally across all records jointly.

The Financial Epistemic Integrity condition is not a new regulatory standard per se, although labelling it as such in this paper is useful for its application in the future. It is a formalisation of what financial data has always been required to be, expressed in terms precise enough to evaluate whether a given processing system is capable of producing records that satisfy it. The value of the formalisation lies precisely in this evaluative function. Once FEI is stated precisely, it becomes possible to ask, rigorously, whether any given class of AI system is architecturally capable of satisfying it. Section 3 and Section 4 address that question directly.

Two observations about the FEI condition are worth making before proceeding. First, FEI is a binary property, not a matter of degree. A record either satisfies all three conditions or it does not. There is no partial FEI, no approximately compliant financial record, no acceptable level of contamination. This follows directly from the conservation law: a financial state that partially satisfies the conservation constraint is not a financial state - it is a defective data structure. Second, FEI applies to the processing system, not merely to the output. A financial record that happens to be numerically correct but whose derivation is not traceable fails FEI regardless of its accuracy, because the audit verifiability property is violated. This point is of fundamental importance for the argument that follows: the question is not whether a probabilistic AI system sometimes produces correct financial outputs. It is whether the system’s architecture is capable of producing outputs that satisfy all three FEI conditions simultaneously. Section 4 proves that it is not.

3. The Stochastic Contamination Framework

The term contamination is chosen deliberately. In chemistry and biology, contamination describes the introduction of a foreign substance into a system in a way that alters the system’s properties and cannot be reversed by removing the contaminant after the fact, because the contaminant has already interacted with and changed the host system. Financial data contamination works by an analogous mechanism. Once probabilistic uncertainty is introduced into a financial data system at a point where it cannot be detected, the downstream records derived from that point carry the uncertainty forward, and removing it requires not merely correcting the contaminated record but re-deriving every subsequent record that depended on it from source. In a financial system of any complexity, this is equivalent to reconstructing the entire financial history from primary documents. The contamination is not a stain that can be wiped away in the same way that you cannot return a cake to it’s source ingredients. It is a structural alteration that propagates through the system’s conserved state.

This section defines Stochastic Contamination precisely, establishes its conditions of occurrence, identifies its distinguishing properties, and demonstrates why it is irrecoverable within standard audit and compliance architectures. The formal proof of its incompatibility with probabilistic AI systems is reserved for Section 4.

3.1 Definition of Stochastic Contamination

Stochastic Contamination is defined as follows:

A financial data system S is stochastically contaminated at time t if there exists at least one record R admitted into S at or before time t such that:

(i) R was produced by a process that does not preserve a deterministic, traceable derivation chain from primary source evidence to output; and

(ii) The probabilistic uncertainty introduced by that process is not represented within R or within the audit trail of S in a form that permits its identification, quantification, or isolation.

Several features of this definition require explicit commentary.

First, the definition does not require that R be numerically incorrect. A record produced by a probabilistic process may happen to contain the correct figures. The contamination occurs regardless, because the audit verifiability property of FEI requires not merely correct outputs but traceable derivations. A correct output without a traceable derivation is a contaminated record in the sense defined here, because its correctness cannot be established by audit without independent re-derivation from source.

Second, the definition requires that the uncertainty be unrepresented in the audit trail. This condition distinguishes Stochastic Contamination from ordinary uncertainty, which financial systems handle through provisions, estimates, and disclosures. A provision for doubtful debts introduces uncertainty into a financial system, but that uncertainty is explicitly quantified, disclosed, and subject to audit scrutiny. Stochastic Contamination is uncertainty that enters the system invisibly, without disclosure, and without any mechanism within the standard audit architecture for its detection.

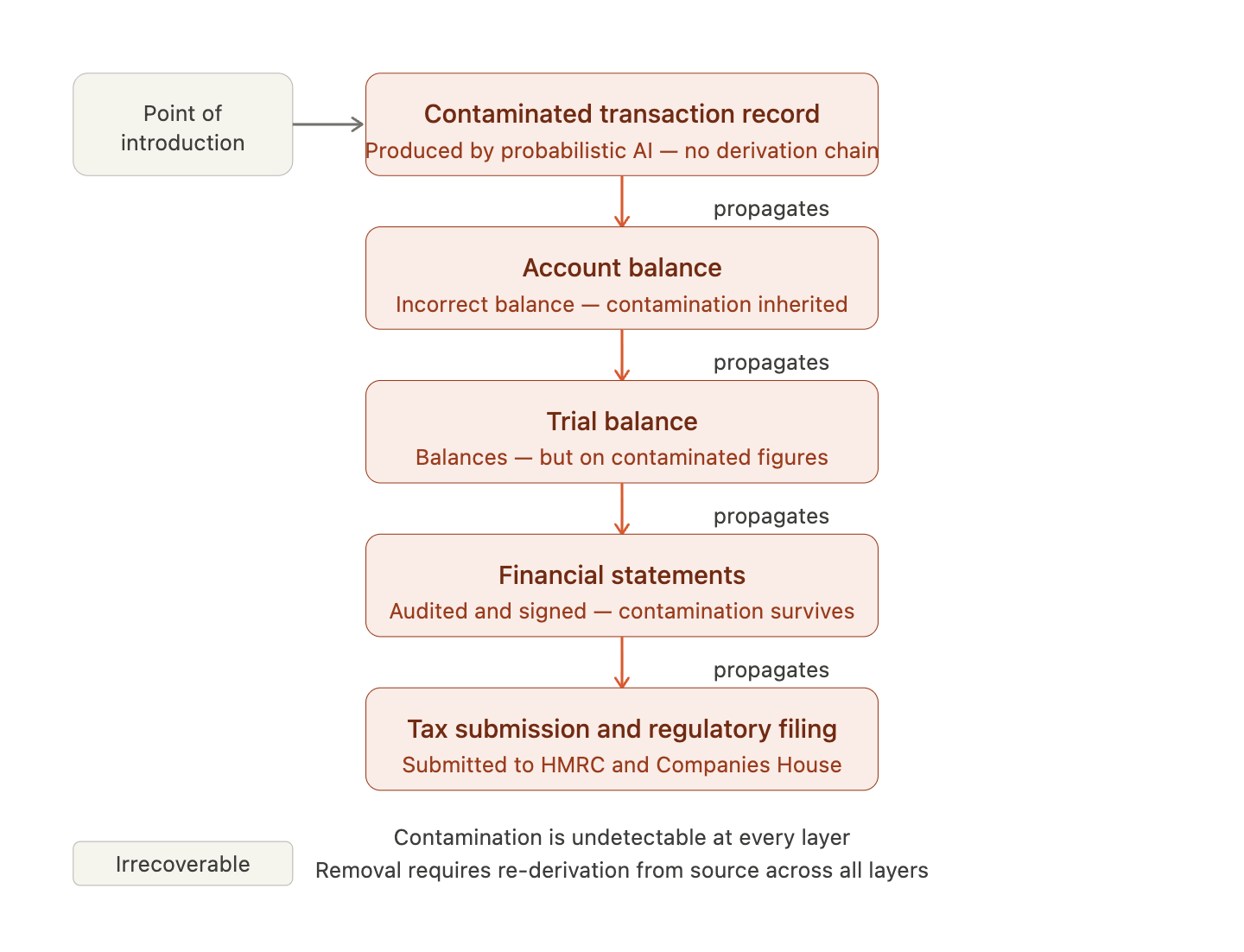

Third, the definition is cumulative. Once a contaminated record is admitted into a financial system, every subsequent record derived from it inherits the contamination. Because the conservation property requires global consistency across the financial state, a contaminated record does not remain locally isolated. It affects every balance, every report, and every submission that draws on the financial state of which it forms part. Contamination at the transaction level propagates to account level, to trial balance level, to financial statement level, to regulatory submission level, in a chain that is as deterministic as the conservation law itself.

3.2 Conditions of Occurrence

Stochastic Contamination occurs when three conditions are jointly satisfied.

The first condition is probabilistic output generation. The processing system produces its output through a mechanism that involves stochastic elements, meaning that the output is a function of a probability distribution over possible outputs rather than a deterministic function of the input. This condition is satisfied by any system whose output cannot be fully predicted from its inputs without knowledge of the random seed or sampling process used during generation.

The second condition is absence of derivation traceability. The processing system does not produce, as a byproduct of its output generation, a step-by-step record of how the output was derived from the input. This condition is satisfied whenever the mapping from input to output involves intermediate computational states that are not stored, not auditable, and not recoverable after the fact.

The third condition is admission into the financial state. The output of the probabilistic system is admitted into the financial data system as a financial record, meaning that it becomes part of the accepted financial state against which balances are calculated, reports are produced, and regulatory submissions are made.

When all three conditions are jointly satisfied, Stochastic Contamination occurs. The conditions are jointly necessary: a probabilistic system that does not produce outputs admitted into the financial state does not contaminate it, and a system that produces outputs admitted into the financial state but does so through a deterministic and traceable process does not produce contamination in the sense defined here. The contamination is a product of the specific combination of probabilistic generation and financial state admission without derivation traceability.

3.3 The Undetectability Property

The most consequential feature of Stochastic Contamination, and the feature that distinguishes it from ordinary financial error, is its undetectability within standard audit and compliance architectures. This property requires careful elaboration because it is counterintuitive: if a record is wrong, why cannot an auditor detect the error?

The answer is that audit, as currently practised under International Standards on Auditing and equivalent national frameworks, is a sampling and evidence-based procedure, not an exhaustive verification. Auditors do not verify every financial record independently from source. They assess risk, select samples, examine evidence for selected items, and form a judgment about the overall reliability of the financial statements. This approach is rational given the volume of transactions in any significant financial entity and the cost of exhaustive verification. It works because the errors it is designed to catch, human processing errors, misclassifications, omissions, duplicate entries, have detectable signatures. They produce inconsistencies with source documents, violations of the conservation constraint, implausible patterns in account balances, or anomalies that risk assessment procedures are designed to identify.

Stochastic Contamination does not have these signatures. A contaminated record produced by a probabilistic AI system may be fully consistent with the conservation constraint, because the system may have correctly maintained the accounting equation while misclassifying the nature of a transaction. It may be consistent with the source document presented to the auditor, because the system may have processed the document but assigned it to an incorrect category in a way that is not apparent from the document itself. It may produce no anomalies in account balance patterns, because the misclassification may be systematic rather than random, producing internally consistent but incorrect accounts. It will not produce an audit trail inconsistency, because the probabilistic system does not produce an audit trail at all in the sense required by FEI. There is nothing for the auditor’s standard procedures to catch.

It is important to understand that the undetectability of Stochastic Contamination is not a temporary limitation of current audit technology. It is a structural consequence of the mismatch between how probabilistic systems generate outputs and what audit procedures are designed to detect. Audit procedures detect deviations from expected patterns in human-produced financial data. Probabilistic AI systems produce outputs that are specifically optimised to be plausible and pattern-consistent, because that is what their training process rewards. The more capable the probabilistic AI system, the more plausible its contaminated outputs, and therefore the less detectable the contamination.

3.4 The Irrecoverability Property

The second distinguishing feature of Stochastic Contamination is its irrecoverability within standard financial and audit architectures. Once a contaminated record has been admitted into the financial state and downstream records have been derived from it, removing the contamination requires identifying the contaminated record, which the undetectability property establishes cannot be done through standard audit procedures, and re-deriving every subsequent record that depended on it from source, which requires access to primary source documents and the processing capacity to reconstruct the financial history.

In practice, irrecoverability means that a financial system that has admitted contaminated records is in a state where the boundary between its reliable and unreliable records cannot be established without exhaustive re-verification from source. Importantly, this is not a proportionate or scalable response to a routine processing error, but the financial equivalent of a database corruption event, requiring full reconstruction rather than targeted correction. For a financial entity of any significant size, this is operationally equivalent to irreversibility.

The irrecoverability property has a temporal dimension that amplifies its consequences. Financial records do not exist in isolation. They are the basis for subsequent transactions, for period-end reporting, for tax submissions, for loan covenant calculations, for audit sign-off, and for the published financial statements on which investors, creditors, employees, and counterparties rely. Each of these downstream uses creates a new layer of records and decisions derived from the contaminated financial state. As time passes, the contamination does not becomes less detectable and more deeply embedded in the financial history of the entity and in the decisions of the parties who relied on that history. The irrecoverability of the original contamination compounds with every subsequent use of the contaminated financial state.

3.5 Stochastic Contamination and the FEI Condition

The relationship between Stochastic Contamination and the Financial Epistemic Integrity condition established in Section 2 is direct and formal. Stochastic Contamination violates FEI at the level of each of the three properties.

It violates the mathematical conservation property not necessarily by breaking the accounting equation in any individual record, but by breaking the global guarantee that the conservation constraint is satisfied across all records simultaneously. A financial state that contains contaminated records is one in which the satisfaction of the conservation constraint cannot be established without exhaustive verification, because some records in the system were produced by a process that does not guarantee conservation preservation by construction.

It violates the legal obligation property by producing records whose demonstrable correctness cannot be established, because there is no traceable derivation from source evidence that an auditor, regulator, or court can inspect and confirm. A contaminated record may be numerically correct, but it is legally deficient in the sense established in Section 2.2, because its correctness is asserted rather than demonstrated.

It violates the audit verifiability property directly and completely, because the audit trail condition requires an unbroken, step-by-step derivation chain from source to output, and probabilistic generative systems do not produce such chains. The contamination is not a gap in the audit trail. It is the complete absence of the audit trail at the point of the contaminated record, with consequences for every downstream record derived from it.

The formal proof that probabilistic AI systems necessarily produce Stochastic Contamination when operating on financial data, and therefore necessarily violate FEI, is the subject of Section 4.

4. The Stochastic Contamination Theorem

This section states and proves the central formal claim of this paper: that any probabilistic AI system operating on financial data necessarily produces Stochastic Contamination as defined in Section 3, and therefore necessarily violates the Financial Epistemic Integrity condition established in Section 2. The proof is constructive, proceeding from the architectural properties of probabilistic AI systems through the three conditions of Stochastic Contamination to the violation of each FEI property in turn.

4.1 Preliminary Definitions

Let F be a financial data system satisfying the Financial Epistemic Integrity condition as defined in Section 2.4. Let A be a probabilistic AI system with the following properties:

P1 (Stochastic output generation): The output of A is a function of a probability distribution over possible outputs. Formally, for any input x, A produces output y drawn from a conditional probability distribution P(y | x; θ), where θ represents the parameters of A. The output y is not a deterministic function of x: for identical inputs x, A may produce different outputs y across runs.

P2 (Absence of derivation traceability): A does not produce, as a component of its output, a step-by-step derivation chain mapping x to y through auditable intermediate states. The mapping from x to y involves intermediate computational states that are neither stored nor recoverable after the output y is generated.

P3 (Finite output vocabulary): A generates its output by sampling from a distribution over a finite vocabulary V of tokens, composing output y as a sequence y = (v₁, v₂, ..., vₙ) where each vᵢ ∈ V is drawn sequentially from P(vᵢ | v₁, ..., vᵢ₋₁, x; θ).

Properties P1 through P3 are satisfied by all transformer-based large language models as a consequence of their architecture (Vaswani et al., 2017). They are also satisfied by a broader class of probabilistic generative systems including diffusion models, variational autoencoders, and stochastic neural networks. The theorem is stated for probabilistic AI systems generally and applied specifically to transformer-based large language models in Section 5.

Let R_A denote a financial record produced by A operating on financial input data, and let S_A denote the financial data system that results from admitting R_A into F.

4.2 The Stochastic Contamination Theorem

Theorem (Stochastic Contamination): Let F be a financial data system satisfying FEI and let A be a probabilistic AI system satisfying properties P1, P2, and P3. If A operates on financial data drawn from F and produces output that is admitted into F as a financial record R_A, then S_A is stochastically contaminated in the sense of Definition 3.1, and S_A does not satisfy FEI.

Proof:

The proof proceeds in three parts, corresponding to the three conditions of Stochastic Contamination in Definition 3.1 and the three properties of FEI in Section 2.4.

Part I: R_A was produced by a process that does not preserve a deterministic, traceable derivation chain (Contamination Condition i).

By property P1, A produces its output y by sampling from the conditional distribution P(y | x; θ). The output y is therefore a realisation of a random variable, not a deterministic function of x. This means there exists no function g such that y = g(x) for all inputs x; rather, y ~ P(y | x; θ), meaning different outputs may be produced from identical inputs depending on the random seed employed at sampling time.

By property P3, A produces y sequentially, where each token vᵢ is drawn from P(vᵢ | v₁, ..., vᵢ₋₁, x; θ). The probability assigned to each token at each position is a function of the entire preceding context and the model parameters θ, but the specific token selected is determined by a sampling process that introduces stochasticity. Even in the limiting case of deterministic decoding, where argmax selection is used rather than stochastic sampling, the output is still a function of learned parameters θ rather than a deterministic logical derivation from input data, and therefore fails the derivation traceability requirement of FEI condition (iii). It is worth noting that the case of deterministic decoding, where argmax selection is used rather than stochastic sampling, does not escape this conclusion. Under argmax decoding P1 is technically weakened: the output becomes a deterministic function of the input given fixed parameters θ. However, the proof of Contamination Condition (i) does not depend on P1 alone. Even where output generation is deterministic, P2 is independently sufficient: the absence of an auditable intermediate state record mapping x to y means that no traceable derivation chain exists regardless of whether the output generation process is stochastic or deterministic. The argmax case therefore satisfies Contamination Condition (i) through P2 alone, and the stochasticity established by P1 and P3 is not necessary for this conclusion, though it strengthens it in the general case.

By property P2, A does not produce an auditable intermediate state record mapping x to y. The intermediate computational states through which A passes in generating y, specifically the attention weight matrices, the key-value computations across transformer layers, and the probability distributions over the vocabulary at each generation step, are transient and are not preserved in the output R_A or in any associated record that would constitute an audit trail in the sense required by the audit verifiability property of FEI.

Therefore, R_A was produced by a process that does not preserve a deterministic, traceable derivation chain from primary source evidence to output. Contamination Condition (i) is satisfied. A further clarification is required to connect the absence of a logical derivation function to the absence of a traceable chain from primary source evidence, as required by Contamination Condition (i). A traceable derivation chain from primary source evidence requires that every step of the derivation can be independently verified against that evidence by a third party without access to the system that produced the output. A statistical function mapping input tokens to a probability distribution over output tokens, and selecting the output by sampling from that distribution, cannot satisfy this requirement: its intermediate states are parameterised by θ, which encodes patterns learned from training data rather than logical rules applied to the specific source evidence presented at inference time. The derivation of R_A from source evidence E is therefore untraceable not merely because P2 establishes that intermediate states are not preserved, but because even if those states were preserved, they would not constitute a chain connecting E to R_A through logical steps that can be independently verified against E. The statistical function and the source-evidence derivation chain are categorically distinct objects.

Part II: The probabilistic uncertainty introduced by A is not represented within R_A or within the audit trail of S_A in a form that permits its identification, quantification, or isolation (Contamination Condition ii).

The output R_A produced by A takes the form of a financial record: a transaction classification, an account posting, a balance figure, or similar. Financial records of these types do not carry probability distributions as part of their structure. A financial record states that a transaction is classified as expense category C, or that account balance B has value V. It does not and cannot, within the structure of a financial record as defined by accounting standards and regulatory requirements, state that the classification has probability p₁ of being correct and probability 1-p₁ of being incorrect.

This is not a contingent limitation of current accounting software. It is a structural property of financial records as legal documents. A filed tax return, a Companies House filing, a balance sheet submitted under the Companies Act 2006, or a record produced for HMRC under Making Tax Digital cannot contain probability distributions over possible correct values. The legal framework requires that these documents assert specific figures as accurate representations of the financial state. A document that asserted a figure as probably correct would fail the legal obligation property of FEI and would not constitute a valid financial record.

Consequently, the probabilistic uncertainty inherent in R_A by virtue of P1, the fact that A’s output is a sample from a distribution rather than a deterministic derivation, is necessarily stripped from R_A at the point of its admission into F. The uncertainty is present in A’s generation process but absent from the record that enters the financial data system. Nothing in the audit trail of S_A represents this uncertainty, because the audit trail records only the admitted financial records and their derivation chains, and R_A carries no derivation chain that would permit the uncertainty to be reconstructed.

Therefore, the probabilistic uncertainty introduced by A is unrepresented in R_A and in the audit trail of S_A. Contamination Condition (ii) is satisfied.

Part III: S_A does not satisfy FEI.

Since both conditions of Stochastic Contamination are satisfied, S_A is stochastically contaminated by Definition 3.1. It remains to show that S_A does not satisfy FEI. This follows directly from the three FEI properties.

FEI property (i), the mathematical conservation property, requires that all records in S_A are consistent with the conservation constraint. Since R_A was produced by a process that does not guarantee conservation preservation by construction, the conservation constraint cannot be established to hold across S_A without exhaustive independent re-verification of R_A from source data. The conservation property of S_A is therefore unestablished, which is distinct from established and is sufficient to constitute a violation of FEI property (i). This conclusion requires one further clarification. A reviewer might observe that a probabilistic system could happen to produce outputs that preserve conservation even without architectural guarantees, and ask whether this constitutes satisfaction of FEI property (i) in practice. It does not, for the reason established in Section 2.1: FEI property (i) requires conservation by architectural construction, meaning the system must be designed such that no non-conserving output can enter the accepted financial state. Conservation by coincidence, where the system produces a conserving output in a given instance without any architectural mechanism preventing non-conserving outputs in other instances, does not satisfy the property. The FEI condition requires a guarantee, not an outcome. A probabilistic system that happens to produce conserving outputs on some or all runs provides no such guarantee, because its architecture permits non-conserving outputs and the occurrence of a conserving output in any given run does not establish that conservation will hold across the system as a whole.

FEI property (ii), the legal obligation property, requires that there exists a set of accessible and auditable source evidence E such that the correctness of R_A can be established by reference to E. By Part I, R_A was produced by a stochastic sampling process rather than a deterministic derivation from E. Therefore, reference to E alone cannot establish the correctness of R_A: even if E is consistent with R_A, an auditor examining E cannot determine whether A would always produce R_A from E, since by P1 A may produce different outputs from identical inputs. The demonstrability requirement of the legal obligation property is therefore violated.

FEI property (iii), the audit verifiability property, requires that the derivation of R_A from source evidence is traceable through an unbroken, step-by-step chain that is itself auditable. By Part I and Part II, no such chain exists for R_A: the derivation involves stochastic intermediate states that are not recorded and cannot be reconstructed. The audit trail condition is therefore violated directly and completely.

Since R_A violates all three FEI properties, S_A does not satisfy FEI. By the conservation propagation property established in Section 2.1, the violation propagates to every record in S_A that is derived from or affected by R_A.

4.3 Corollaries

Three corollaries follow directly from the theorem.

Corollary 1 (Independence from numerical accuracy): Stochastic Contamination of S_A occurs regardless of whether R_A is numerically correct. The theorem does not require that A produce an incorrect output. It requires only that A’s output be produced by a process satisfying P1, P2, and P3. A numerically correct output produced by such a process is still a contaminated record because it violates FEI properties (ii) and (iii) independently of its numerical content.

Corollary 2 (Independence from system capability): Stochastic Contamination occurs regardless of the capability or accuracy of A. A more capable probabilistic AI system, one with lower average error rates, higher factual accuracy, or better domain calibration, does not reduce the contamination it introduces into F. The contamination is a property of the interaction between the architectural properties P1, P2, and P3 and the FEI requirements, not of the system’s performance on accuracy benchmarks.

Corollary 3 (Irrecoverability): Once S_A is stochastically contaminated, the contamination cannot be removed without identifying all contaminated records, which requires exhaustive re-verification from source, and re-deriving every subsequent record that depended on them, which requires reconstructing the financial history. In a financial system of any practical complexity, this is operationally equivalent to irreversibility.

4.4 Scope of the Theorem

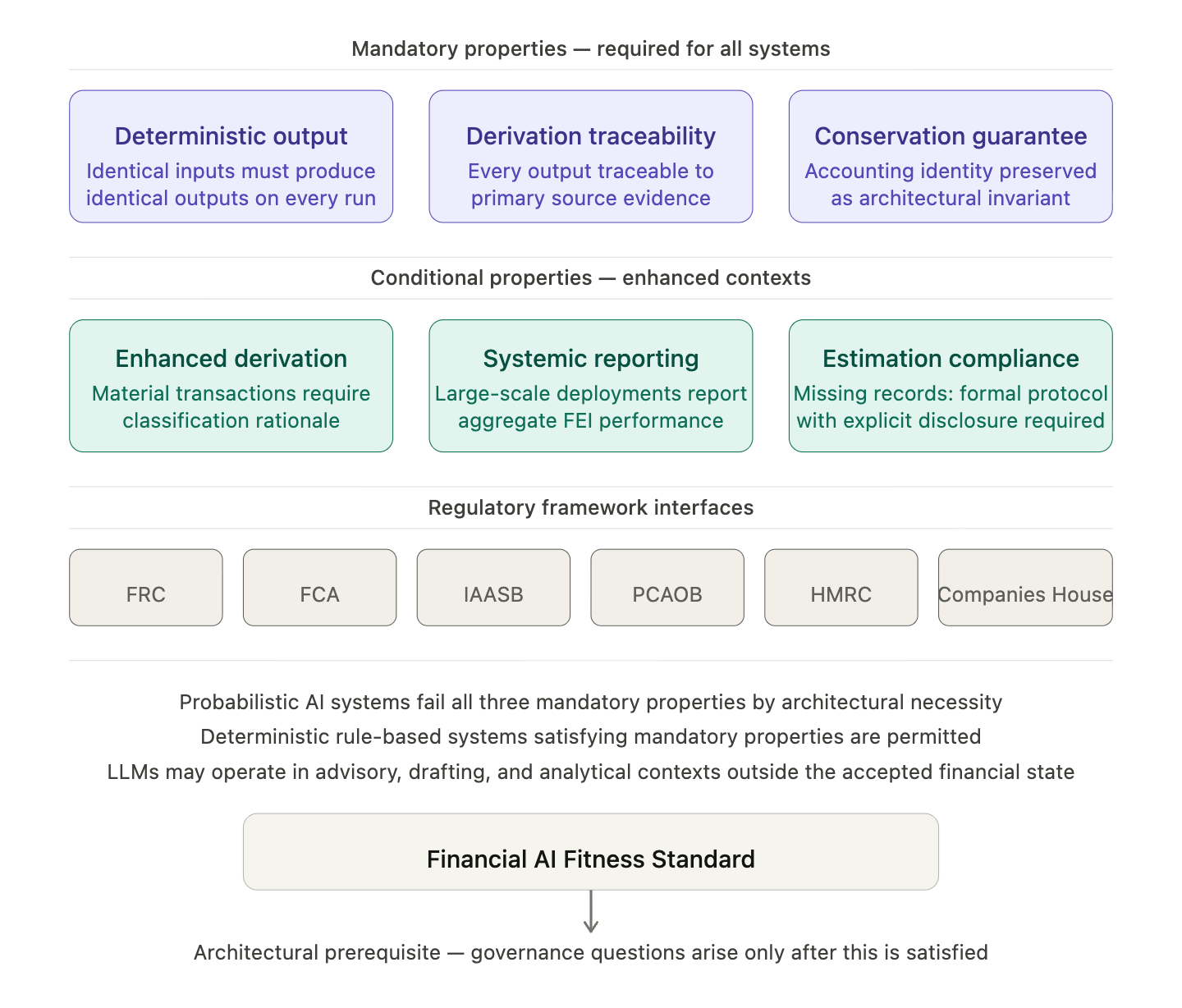

The theorem applies to all probabilistic AI systems satisfying P1, P2, and P3, and therefore applies to large language models, diffusion-based financial document processors, stochastic neural classifiers, and any other system whose outputs are samples from a learned probability distribution rather than deterministic derivations from input data. The theorem does not apply to fully deterministic rule-based systems whose outputs are logical functions of structured input data and whose derivation chains are fully auditable. The governance implication is therefore not that AI must be excluded from financial data processing. It is that only AI systems that do not satisfy P1, P2, and P3, that is, systems that are fully deterministic, fully traceable, and free of stochastic output generation, are architecturally compatible with the Financial Epistemic Integrity condition.

Section 5 applies this result specifically to large language models, examining why the architectural properties of transformer-based systems satisfy P1, P2, and P3 by construction and why proposed mitigations, retrieval augmented generation, domain fine-tuning, and constitutional constraints, do not alter this conclusion.

5. Why Large Language Models Are Architecturally Disqualified

The Stochastic Contamination Theorem proved in Section 4 applies to all probabilistic AI systems satisfying properties P1, P2, and P3. This section applies the theorem specifically to transformer-based large language models, which are the class of probabilistic AI system most actively being deployed in financial services contexts. The section proceeds in four parts: first, demonstrating that LLMs satisfy P1, P2, and P3 by architectural necessity; second, examining the three principal mitigation strategies proposed by the industry and demonstrating why none of them resolves the contamination problem; third, addressing the argument that sufficiently capable LLMs might achieve effective determinism through high accuracy; and fourth, establishing why the disqualification is permanent under the transformer architecture rather than a limitation of current model capability.

5.1 How LLMs Satisfy the Contamination Conditions by Construction

A transformer-based large language model operates as follows. Given an input sequence of tokens x = (x₁, x₂, ..., xₙ), the model computes a sequence of contextualised representations through multiple layers of multi-headed self-attention and feed-forward transformations. At each generation step, these representations are projected onto a probability distribution over the vocabulary V through a softmax function, and the next token is selected by sampling from this distribution (Vaswani et al., 2017). The output is built token by token, with each token selection conditional on all previously selected tokens and the original input.

This architecture satisfies property P1 directly and by construction. The softmax projection produces a probability distribution over all tokens in V at every generation step, meaning the output is fundamentally a sample from a probability distribution rather than a deterministic function of the input. Even in the limiting case where temperature is set to zero and argmax decoding is used, the output remains a function of learned statistical parameters θ that were estimated from training data rather than a logical derivation from the specific input presented at inference time. The distinction is fundamental: a logical derivation produces an output that is correct by construction given correct premises; a statistical estimation produces an output that is probable given training data, which is not the same thing and does not satisfy the same verifiability requirements.

Property P2 is satisfied because the intermediate computational states through which the transformer passes in generating its output, specifically the attention weight matrices at each layer, the key-value computations, and the token probability distributions at each generation step, are transient computational artifacts that are discarded after the output is produced. They are not preserved as part of the output, not stored as an audit trail, and not recoverable from the output after the fact. The output of an LLM is a token sequence. It does not carry with it the chain of intermediate computations that produced it, and there is no mechanism within the standard transformer architecture for producing such a chain in the form required by the audit trail condition of FEI.

Property P3 is satisfied definitionally, as sequential token sampling over a finite vocabulary is the fundamental generative mechanism of transformer-based language models.

Since LLMs satisfy P1, P2, and P3 by construction, the Stochastic Contamination Theorem applies directly: any LLM operating on financial data and producing outputs admitted into a financial data system as financial records will stochastically contaminate that system and violate the Financial Epistemic Integrity condition.

5.2 Why Retrieval Augmented Generation Does Not Resolve the Problem

Retrieval augmented generation (RAG) is the most widely cited mitigation strategy for LLM deployment in financial contexts. RAG architectures augment the LLM’s generation process with a retrieval component that fetches relevant documents from an external knowledge base and provides them as context during generation. The intuition is that grounding the model’s output in retrieved documents reduces its reliance on potentially stale or incorrect parametric knowledge, thereby reducing hallucination rates.

The empirical record on RAG’s effectiveness is instructive. Research published at ICLR 2025 found that RAG models can still produce hallucinations by generating outputs that conflict with the retrieved information, even when that information is accurate and relevant, because the generation process continues to balance parametric knowledge against retrieved context through the same attention mechanism that governs all transformer generation (Sun et al., 2025). Research on financial domain RAG systems has documented temporal inconsistencies in which models correctly retrieve a financial figure but associate it with the wrong date or entity, producing a contaminated record that is internally consistent but factually wrong (arXiv:2602.05723, 2026). The hallucination rate in the best-performing RAG configurations across clinical and financial domains remains measurable and non-zero, with self-reflective RAG achieving rates of approximately 5.8% in controlled evaluations (Tan et al., 2025).

The theoretical reason RAG cannot resolve the contamination problem is more fundamental than the empirical evidence alone suggests. RAG reduces the probability that an LLM will generate an incorrect output by providing better context. It does not alter the architecture of the generation process. The LLM in a RAG system still satisfies properties P1, P2, and P3: its outputs are still samples from a probability distribution, its intermediate states are still not preserved as an auditable derivation chain, and its generation is still token-by-token sequential sampling over a finite vocabulary. RAG changes the quality of the inputs to the probabilistic process. It does not make the process deterministic, and it does not produce a derivation chain from retrieved documents to output that satisfies the audit trail condition of FEI.

The contamination problem, as defined in Section 3, is not that LLMs produce incorrect outputs too frequently. It is that their outputs lack the derivation traceability required by the Financial Epistemic Integrity condition, regardless of their accuracy. A RAG system that produces a correct financial record 99.9% of the time still produces, on every run, an output without a traceable derivation chain, and therefore still produces Stochastic Contamination on every run. The correctness rate is irrelevant to the contamination. The architecture is determinative.

5.3 Why Domain Fine-Tuning Does Not Resolve the Problem

Domain fine-tuning adapts a pre-trained LLM to a specific domain by continuing its training on domain-specific data. Financial LLMs fine-tuned on accounting standards, regulatory documents, company filings, and transaction records have been shown to improve performance on domain-specific tasks and reduce certain categories of hallucination. The argument for fine-tuning in financial contexts is that a model deeply trained on financial data will develop better calibrated probability distributions over financial content, producing outputs that are more reliably correct.

The empirical finding that undermines this argument is precisely documented in the literature: fine-tuning on novel information can initially decrease hallucination rates only for them to subsequently increase, a phenomenon known as knowledge instability that results from the tension between new domain knowledge and the model’s existing parametric knowledge (Gekhman et al., 2024). More fundamentally, the theoretical literature has established that for broad classes of language generation tasks, any model that generalises beyond its training data will either hallucinate invalid outputs or suffer mode collapse, failing to produce the full range of valid responses (Kleinberg and Mullainathan, 2024). Fine-tuning does not eliminate this fundamental trade-off. It shifts the model’s performance characteristics within the space defined by it.

The theoretical reason fine-tuning cannot resolve the contamination problem is identical to the reason RAG cannot: it does not alter the architectural properties P1, P2, and P3 that cause Stochastic Contamination. A fine-tuned LLM still generates outputs by sampling from a probability distribution over a vocabulary. It still produces no auditable derivation chain from input to output. It still satisfies all three properties that the theorem proves are sufficient for Stochastic Contamination. Fine-tuning changes the parameters θ of the model, not the architecture of its generation process, and it is the architecture of the generation process, not the values of θ, that produces the contamination.

5.4 Why Constitutional Constraints Do Not Resolve the Problem

Constitutional AI and related constraint mechanisms impose rules on LLM output through training objectives, output filtering, or post-processing verification. The idea is that an LLM constrained to follow certain principles, including accuracy principles and domain-specific rules, will produce outputs that are more reliable and more consistent with established facts. Some financial AI deployments implement verification layers that check LLM outputs against structured databases before admitting them into downstream systems.

Constitutional constraints can reduce the frequency of certain categories of hallucinated output. They cannot resolve the contamination problem for two reasons. First, the verification mechanism that checks LLM outputs against a database is itself performing a comparison between two data objects: the LLM’s output and the database record. Where the two agree, the verification passes the output. Where they disagree, the output is rejected or flagged. But this mechanism only catches contamination that produces a result inconsistent with the database. Contamination that produces a plausible, database-consistent but incorrect result, for example a transaction classified in an adjacent but incorrect category, is invisible to the verification layer. The verification checks consistency, not derivation.

Second, and more fundamentally, the post-processing verification mechanism does not produce an auditable derivation chain from source data to output in the sense required by FEI property (iii). It produces a record that an output passed a consistency check. This is not the same as a record that an output was derived from source data through an auditable logical process. A financial record that passed a consistency check against a database is not a financially valid record in the FEI sense. It is a record that was found to be consistent with another record, which is a weaker property that does not satisfy the audit trail condition.

5.5 The Capability Fallacy

A common response to the disqualification argument is that as LLMs become more capable, their effective error rate approaches zero, and at sufficiently low error rates the contamination risk becomes negligible. This argument confuses accuracy with verifiability and misunderstands the nature of the Financial Epistemic Integrity condition.

FEI is a binary property. A financial record either has a traceable derivation from source data or it does not. The frequency with which an LLM produces numerically correct outputs is irrelevant to whether those outputs have traceable derivations, because the absence of a derivation chain is an architectural property of the generation process, not a property of any individual output. A highly capable LLM that produces correct financial records 99.99% of the time produces, on every single run, outputs without traceable derivation chains. Every one of those outputs is a contaminated record in the sense defined in Section 3, because Corollary 1 of the theorem establishes that Stochastic Contamination is independent of numerical accuracy.

The capability fallacy is particularly dangerous in the financial context because it provides a seemingly rational basis for deploying LLMs in financial data processing while dismissing contamination concerns as theoretical. It is not theoretical. As demonstrated empirically by research finding that broad classes of language models face a fundamental trade-off between hallucination and mode collapse that cannot be escaped through capability improvement alone (Kleinberg and Mullainathan, 2024), the contamination problem is not a function of insufficient capability. It is a function of architecture. Increasing capability makes the contamination less frequent. It does not make the contamination detectable, recoverable, or compatible with the Financial Epistemic Integrity condition.

5.6 The Permanent Nature of the Disqualification

The disqualification of LLMs from financial data processing is not a temporary limitation pending further research or development. It is a permanent consequence of the transformer architecture as long as that architecture generates outputs through probabilistic token sampling rather than deterministic logical derivation.

A transformer-based LLM that generated outputs through deterministic logical derivation would not be an LLM in any meaningful sense. It would be a rule-based system with a natural language interface: a system that applies explicit logical rules to structured inputs and produces outputs that are traceable to those rules. Such a system might be architecturally compatible with the Financial Epistemic Integrity condition, and might constitute a useful tool in financial data processing, but it would not be a large language model. The capability that makes LLMs valuable, their ability to generalise across contexts, synthesise information from diverse sources, and generate fluent and contextually appropriate responses to novel inputs, is a direct consequence of the probabilistic architecture that produces Stochastic Contamination. It is not possible to preserve the former while eliminating the latter within the transformer architecture. The disqualification and the capability are the same thing, seen from different perspectives.

This is the conclusion that the financial services industry, the accounting profession, and their regulators have not yet confronted directly. The question is not how to make LLMs safe enough to use in financial data processing. The question is what class of system should be used instead, and what properties that system must have to satisfy the Financial Epistemic Integrity condition. Section 8 addresses the first question through the live case. Section 9 addresses the second through the Financial AI Fitness Standard.

6. The Regulatory Gap

The Stochastic Contamination Theorem establishes that probabilistic AI systems operating on financial data necessarily violate the Financial Epistemic Integrity condition. The regulatory frameworks governing AI in financial contexts do not contain this finding, do not reflect the conceptual vocabulary required to act on it, and in several cases are actively encouraging the deployment of precisely the systems that the theorem disqualifies. This section examines each relevant framework in turn, identifies the specific gap in each, and proposes the minimum amendment required to close it.

6.1 The Financial Reporting Council

The FRC published its first guidance on AI in audit in mid-2025, followed by further guidance on generative and agentic AI tools in audit engagements in March 2026 (FRC, 2026). The guidance represents the most substantive regulatory engagement with AI in financial contexts produced by any UK body to date. It addresses risk identification, documentation requirements, human oversight obligations, and quality assurance processes for AI-assisted audit work. It does not make an architectural distinction between probabilistic and deterministic AI systems. Its approach is to identify the risks that generative AI tools introduce and to specify mitigations: human review of AI outputs, documentation of tools used, quality controls over AI-generated work products.

This approach has a structural limitation that the guidance does not acknowledge. The mitigations it specifies, human review of AI outputs and documentation of tools used, address the symptoms of Stochastic Contamination without addressing its cause. As established in Section 3.3, contaminated outputs produced by LLMs are undetectable through standard review procedures precisely because they are designed to be plausible and pattern-consistent. Human review of AI-generated audit work products will not reliably catch contamination that has no surface indicators of error. Documentation of the AI tool used does not produce the derivation chain from source data to output that the audit verifiability property of FEI requires. The FRC’s guidance makes probabilistic AI use in audit safer in the sense of more documented and more scrutinised. It does not make it FEI-compliant.

The gap in the FRC framework is the absence of a requirement that AI systems used in audit engagements produce outputs with auditable derivation chains traceable to source data. Without this requirement, audit firms can deploy LLMs in audit work, document their use, subject their outputs to human review, and remain in compliance with FRC guidance while introducing Stochastic Contamination into the audit process. The amendment required is: the addition to FRC guidance of an explicit requirement that AI systems used in audit engagements satisfy the audit trail condition, meaning that every AI-generated output must be accompanied by an auditable record of the logical steps through which the output was derived from source evidence.

6.2 The Financial Conduct Authority

The FCA has engaged extensively with AI in financial services since 2024, publishing research notes, running an AI lab, conducting a Supercharged Sandbox in partnership with NVIDIA, and soliciting feedback through its AI Input Zone (FCA, 2024; FCA, 2025). Its approach reflects the UK government’s pro-innovation stance: rather than establishing prescriptive requirements, the FCA is applying its existing regulatory principles, consumer duty, operational resilience, model risk management, and systems and controls requirements, to AI deployments case by case.

The FCA’s existing framework contains requirements that are partially relevant to the contamination problem. Consumer duty requires that firms deliver good outcomes for retail customers, which implies that AI systems producing contaminated financial records that lead to incorrect consumer outcomes are in breach. Operational resilience requirements apply to critical AI systems. Model risk management guidance requires firms to understand and manage the risks of models used in decision-making.

None of these requirements, however, prohibits the use of probabilistic AI in financial data processing on architectural grounds or requires that AI outputs be derivation-traceable to source data. The FCA’s framework is outcome-focused rather than architecture-focused: it asks whether AI deployments produce good outcomes rather than whether the architectural properties of the AI system are compatible with the FEI condition. The contamination problem cannot be addressed by outcome monitoring alone, because the undetectability property established in Section 3.3 means that contaminated outcomes are not reliably distinguishable from uncontaminated outcomes through ex post monitoring. By the time contamination is detected, it has propagated through the financial data system and into the downstream decisions that depended on it.

The gap in the FCA framework is the absence of any requirement that AI systems processing financial data in FCA-regulated firms satisfy architectural conditions equivalent to the FEI condition. The amendment required is: the addition to the FCA’s model risk management guidance and consumer duty framework of a requirement that AI systems generating financial records, reports, or assessments satisfy a minimum architecture standard requiring deterministic, auditable derivation chains from source data to output, and that systems not satisfying this standard be prohibited from generating records or assessments admitted directly into financial data systems without independent re-derivation from source.

6.3 The IAASB and International Auditing Standards

The IAASB is conducting a gap analysis of its International Standards on Auditing to assess their alignment with technological developments, including AI (IAASB, 2024). ISA 500 governs audit evidence and requires that audit evidence be sufficient and appropriate, meaning relevant and reliable. ISA 315 governs the identification and assessment of risks of material misstatement and requires auditors to obtain an understanding of the entity and its environment, including its information systems. Neither standard contains requirements specific to AI-generated financial data or to the architectural properties of systems that produce financial records subject to audit.

The IAASB gap analysis, to the extent its results are publicly available, addresses questions of how existing standards apply to AI-assisted audit procedures rather than whether the AI systems being audited satisfy conditions compatible with audit verifiability. This is precisely the wrong question. The question that matters is not whether ISA 500 applies to AI-generated audit evidence. It is whether AI-generated audit evidence can satisfy the reliability requirement of ISA 500 when it was produced by a system that does not preserve an auditable derivation chain from source data to output.

The answer the Stochastic Contamination Theorem provides is that it cannot. AI-generated audit evidence produced by a probabilistic system is not reliable in the ISA 500 sense, regardless of its apparent accuracy, because its reliability cannot be established through reference to an auditable derivation process. The contamination is not a reliability risk that auditors can assess through professional judgment. It is a structural property of the evidence that makes reliability assessment by standard audit procedures impossible.

The gap in the IAASB framework is the absence of a requirement in ISA 500 that audit evidence produced by AI systems must be accompanied by an auditable derivation record establishing its traceability to source. The amendment required is: a revision of ISA 500 to add a reliability criterion specific to AI-generated evidence, requiring that evidence produced by automated systems be accompanied by a derivation record satisfying the audit trail condition, and specifying that evidence produced by probabilistic generative systems without such a record does not satisfy the reliability requirements of the standard.

6.4 The PCAOB

The Public Company Accounting Oversight Board oversees the audits of US public companies and broker-dealers and sets auditing standards applicable to those engagements. PCAOB standards, like IAASB standards, address audit evidence quality through sufficiency and appropriateness requirements without making architectural distinctions between AI system types. The PCAOB has issued alerts and staff guidance on the use of technology in audits, including AI, but these focus on auditor responsibilities in relation to AI-assisted procedures rather than on the properties that AI systems must have to produce evidence compatible with PCAOB audit standards.

The PCAOB gap parallels the IAASB gap: its standards require appropriate audit evidence without specifying that appropriateness, in the context of AI-generated evidence, requires a derivation chain traceable to source data. Given that the Sarbanes-Oxley Act requirements for internal controls over financial reporting depend on the integrity of the financial data those controls govern, and given that contaminated financial data produced by probabilistic AI systems undermines that integrity in ways that standard internal control frameworks are not designed to detect, the PCAOB gap has direct implications for public company financial reporting reliability and investor protection.

The amendment required is equivalent to that proposed for the IAASB: a revision of PCAOB evidence standards to require that AI-generated audit evidence satisfy an auditable derivation requirement, and that probabilistic generative systems be prohibited from producing evidence admitted directly into audit documentation without independent verification from source data.

6.5 HMRC and Making Tax Digital

HMRC’s Making Tax Digital programme requires that businesses keep digital records and submit returns using compatible software. From April 2026, the programme requires self-employed taxpayers and landlords with income above £50,000 to use MTD-compatible software, with the threshold reducing progressively through 2028 (HMRC, 2025). The programme specifies that software must be capable of producing digital records and submitting quarterly updates and returns. It does not specify architectural requirements for the software, and in particular, it neither prohibits the use of probabilistic AI components in MTD-compatible software nor requires that software-generated financial records satisfy the audit trail condition.

HMRC is simultaneously mandating digital record-keeping through MTD and investing in AI-assisted compliance checking through its Connect data analytics system and broader AI transformation programme (HMRC Transformation Roadmap, 2025). HMRC is working with industry to produce principles for AI in tax software, with a software roadmap due in 2026. As of the time of writing, no architectural requirements on the AI systems embedded in MTD-compatible software exist. Software using probabilistic AI components to classify transactions, generate expense descriptions, or produce tax computations can be MTD-compliant while producing stochastically contaminated financial records that HMRC’s own systems cannot distinguish from uncontaminated records.

This creates a situation of particular concern. HMRC’s Connect system identifies compliance risks through pattern analysis of submitted data. Contaminated financial records produced by probabilistic AI are, by the undetectability property established in Section 3.3, pattern-consistent and plausible. They will not reliably trigger Connect’s anomaly detection. HMRC therefore faces the prospect of receiving, at scale, MTD-compliant submissions containing contaminated data that its compliance systems cannot detect, contributing to the tax gap through a mechanism that its current analytical infrastructure is not designed to identify.

The amendment required is: the inclusion in HMRC’s software requirements for MTD-compatible software of an architectural standard specifying that any AI components used in transaction classification, financial record generation, or tax computation must produce outputs with auditable derivation chains traceable to source data, and that probabilistic generative AI components not satisfying this requirement are prohibited from generating financial records admitted directly into MTD submissions.

6.6 Companies House

Companies House, operating under enhanced powers granted by the Economic Crime and Corporate Transparency Act 2023, has developed significant new capabilities to query and remove false, misleading, or incorrect information from the company register (Companies House, 2025). Identity verification requirements have been introduced for directors and persons of significant control, and the registrar has new powers to investigate and strike off companies registered on false bases.

These reforms address the integrity of information submitted to the register through authentication and verification of the identities of those submitting it. They do not address the integrity of the financial information itself, specifically the annual accounts and confirmation statements that companies file, in terms of the processing systems that generated those financial records. A company whose accounts were produced using probabilistic AI-assisted accounting software will file accounts that are Companies House-compliant provided they are filed by a verified director. The contamination in the underlying financial records does not affect Companies House compliance because Companies House has no architectural requirements for the systems that generated the filed accounts.

The Companies House gap is narrower in scope than the other frameworks, but is significant because filed accounts are public documents that underpin credit decisions, investment analysis, supply chain due diligence, and regulatory assessments. Contaminated accounts that are Companies House-compliant are nonetheless unreliable as a basis for the economic decisions that public company filings are designed to support.

The amendment required is: the inclusion in Companies House filing requirements of a data quality standard specifying that accounts produced using AI systems must have been generated by systems satisfying the audit trail condition, and that accounts generated by probabilistic AI systems without auditable derivation chains must be accompanied by a disclosure to that effect.

6.7 The Wider Regulatory Implication

The pattern across all six frameworks is consistent. Each framework addresses the risks of AI in financial contexts through outcome requirements, disclosure obligations, human oversight mandates, and risk management principles. None makes the architectural distinction between probabilistic and deterministic systems that the Stochastic Contamination Theorem establishes is necessary to protect financial data integrity. Each framework is therefore capable of being satisfied by deployments of probabilistic AI systems that are producing Stochastic Contamination in the financial data they process.

The common amendment required across all frameworks is an architectural classification requirement: before specifying what governance, oversight, or disclosure obligations apply to an AI system operating on financial data, regulators must first determine whether the system’s outputs are produced through a deterministic, auditable derivation process or through probabilistic generation. Systems satisfying the former may, subject to appropriate rule set audit and output monitoring requirements, be compatible with the Financial Epistemic Integrity condition. Systems satisfying the latter are not, and should be prohibited from generating financial records admitted directly into financial data systems regardless of their accuracy benchmarks, governance arrangements, or human oversight protocols.